Stocks dipped last week, but there are several reasons why it wasn’t terribly bearish.

- Stocks were overbought.

- The S&P 500 held important levels.

- “Risk-on sectors” were strong.

- “Safe havens” were weak.

- Investors are favoring smaller companies.

- The holidays are coming.

Stocks Were Overbought

Stocks began November with a big rally as confidence returned after the Presidential election. The S&P 500 peaked at 4.6 percent above its 10-day moving average. Aside from the bounce in late March and early April, it was the highest distance above the 10-day MA since the market recovered from the financial crisis in March 2009.

Those kind of readings suggest the market’s moved too far, too fast. But historically more upside usually follows.

The S&P 500 Held Key Levels

The rally in early November pushed the S&P 500 to new record highs above its previous peaks in early September and mid-October. The index also broke a downward-sloping trendline.

Prices have remained in this range since and bounced at levels where they earlier fell. That could suggest old resistance has become new support — a potential sign of confidence increasing.

‘Risk On’ Sectors Rose

Some parts of the stock market are considered “risk-on” sectors, which perform better when the economy is improving. Energy stocks can rally because more people working and traveling boost fuel demand. Industrial stocks can benefit from more construction and manufacturing. Financials often go up because they make more money on loans and fewer borrowers default.

| Biggest Gainers in S&P 500 Last Week | |

| Diamondback Energy (FANG) | +19% |

| L Brands (LB) | +16% |

| Occidental Petroleum (OXY) | +14% |

| TechnipFMC (FTI) | +13% |

| ViacomCBS (VIAC) | +13% |

Those sectors advanced last week. Energy led the charge with a gain of almost 6 percent.

‘Risk Off’ Sectors Fell

Other parts of the market are “safe havens,” which can perform well when the economy struggles. Utilities, health-care and consumer staples usually fall under this umbrella. They declined more than 1 percent last week, a sign investors may be tired of playing it safe.

Other safety plays like gold and silver miners also declined — despite a falling U.S. dollar. (Normally a weak dollar should help precious metals.) A weak dollar and weak gold together are another potential sign of risk appetite.

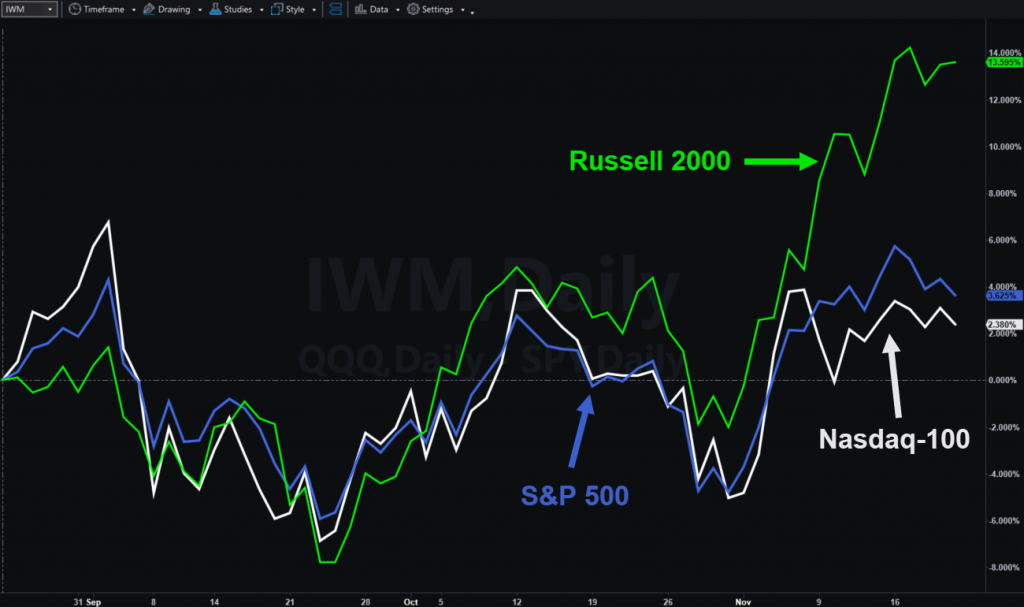

Investors Favored Smaller Companies

A major trend has emerged in the last month: Investors are embracing smaller companies and disregarding big ones.

Megacap names like Apple (AAPL), Amazon.com (AMZN) and Microsoft (MSFT) haven’t made new highs since early September. Meanwhile newer companies like Nio (NIO), Snap (SNAP) and Pinterest (PINS) have set new records in the last month.

This trend is also playing out in the indexes. The small-cap Russell 2000 ETF (IWM) hit new highs last, while the Nasdaq-100 hasn’t made a new high since early September.

The strength in smaller companies also comes at a busy time for initial public offerings (IPOs). Snowflake (SNOW) and Palantir (PLTR) have more than doubled from their IPOs. Now investors are preparing for at least five more big ones: DoorDash, Airbnb, Affirm, Roblox and Wish.

Keep reading Market Insights for more on these deals. Again, strong demand for IPOs is a potential sign of risk appetite and confidence.

| Biggest Decliners in S&P 500 Last Week | |

| Walgreen Boots Alliance (WBA) | -12% |

| Boston Scientific (BSX) | -11% |

| Cardinal Health (CAH) | -10% |

| Centene (CNC) | -8.8% |

| Regeneron Pharmaceuticals (REGN) | -8.4% |

The Holidays Are Coming

Thanksgiving is this week, marking the official start of the holiday-shopping season. Regardless of coronavirus, it’s an important time for the economy and consumers. Confidence tends to rise along with spending and hiring.

Seasonality also favors November, which has seen positive returns for the last eight years straight.

Companies enter the key period with strong momentum financially. A record 84 percent of S&P 500 members beat estimates last earnings season, according to FactSet.

ESG Wave Continues

Last week also saw investors stick with “environmental, social and governance” plays like electric vehicles and solar energy. ESG stocks remain among the best performers this year.

Global equities were strong last week as every major country ETF flew ahead of the S&P 500. Latin American funds did best — another sign of investor confidence.

Busy Week Into Thanksgiving

The next few sessions are very busy, with some events moved forward because of Thanksgiving on Thursday.

Here’s a quick rundown:

- Tomorrow morning: Consumer confidence, plus earnings from Best Buy (BBY), Dick’s Sporting Goods (DKS) and Metronic (MDT).

- Tomorrow afternoon: Earnings from Gap (GPS), HP (HPQ), Nordstom (JWN) and American Eagle Outfitters (AEO).

- Wednesday is huge: Earnings from Deere (DE), plus revised gross domestic product (GDP), initial jobless claims, new-home sales, consumer sentiment, personal income and spending, durable-goods orders, crude-oil inventories and minutes from the last Federal Reserve meeting.

- Thursday: Markets closed.

- Friday: Markets close at 1 p.m. ET.

"last" - Google News

November 23, 2020 at 01:30PM

https://ift.tt/35XaWYE

Last Week's Stock Market Pullback Wasn't Bearish for These 6 Reasons - TradeStation Market Insights

"last" - Google News

https://ift.tt/2rbmsh7

https://ift.tt/2Wq6qvt

Bagikan Berita Ini

0 Response to "Last Week's Stock Market Pullback Wasn't Bearish for These 6 Reasons - TradeStation Market Insights"

Post a Comment